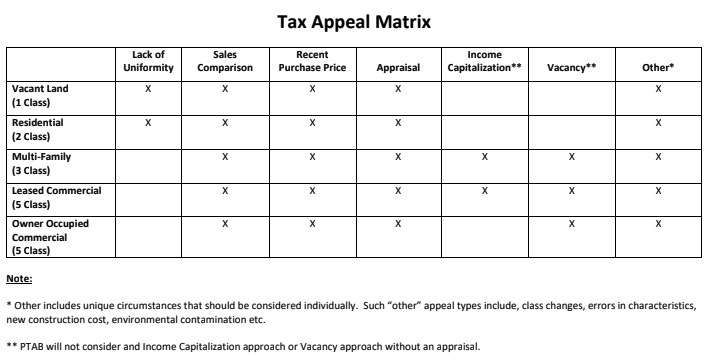

Lack of Uniformity:

Properties are intended to be valued in an equal fashion per assessment metrics. Thus, they are intended to be assessed ‘uniformly’, by law. Determination of assessment equity is made by first calculating the ‘building assessment value per square foot’ of the subject property and then analyzing the same of its comparable properties. If there are a substantial amount of comparables with a lessor ‘building assessment value per square foot’, that serves as an indication of assessment inequity.

Sales Comparison:

What someone is willing to pay is the best indicator of market price. Thus, assessment values are intended to be in-step with the latest sales activity. There is a clause within the tax code that an assessor cannot ‘sales chase’. In other words, they may not increase a properties assessment to be in align with the most recent sales price that’s higher than the established assessment fair market value. However, there isn’t a regulation negating sales chasing downward. The determination of market equity is made by first calculating the ‘market value per square foot’ of the subject property and then analyzing the same of its comparable properties. If there are a substantial amount of comparables with a lessor ‘market value per square foot’, than that of the subject property it serves as an indication of market sales inequity.

Recent Purchase Price:

What someone is willing to pay for a property is the best indicator of market price. Thus, the recent sale of the subject property, within the last 3 years (and non-compulsory), is the best indication of the market price. If a property is assessed at a higher fair-market-value than the latest sales transaction price of the property, then there’s a sale inequity.

Appraisal:

A licensed appraiser is the best officiator of real estate value. If there has been an ad volerem appraisal performed on the subject property within the last 3 years, and of a lessor fair-market-value, then there is a valid case for tax relief.

Income Capitalization:

Estimating the value of an income-producing property is done by a method called Capitalization. Capitalization is any method used to convert an income stream into value and if it’s less than the fair-market-value of that established by the county assessor, then there’s a valid case for tax relief.

Vacancy:

Vacancy refers to the portion of a property building that is not subject to a lease (or from which the owner/landlord is not receiving rental income). Land assessed value is not adjusted based on vacancy evidence. Vacancy reduces the assessed value of a property, which generally reduces the property’s taxes.

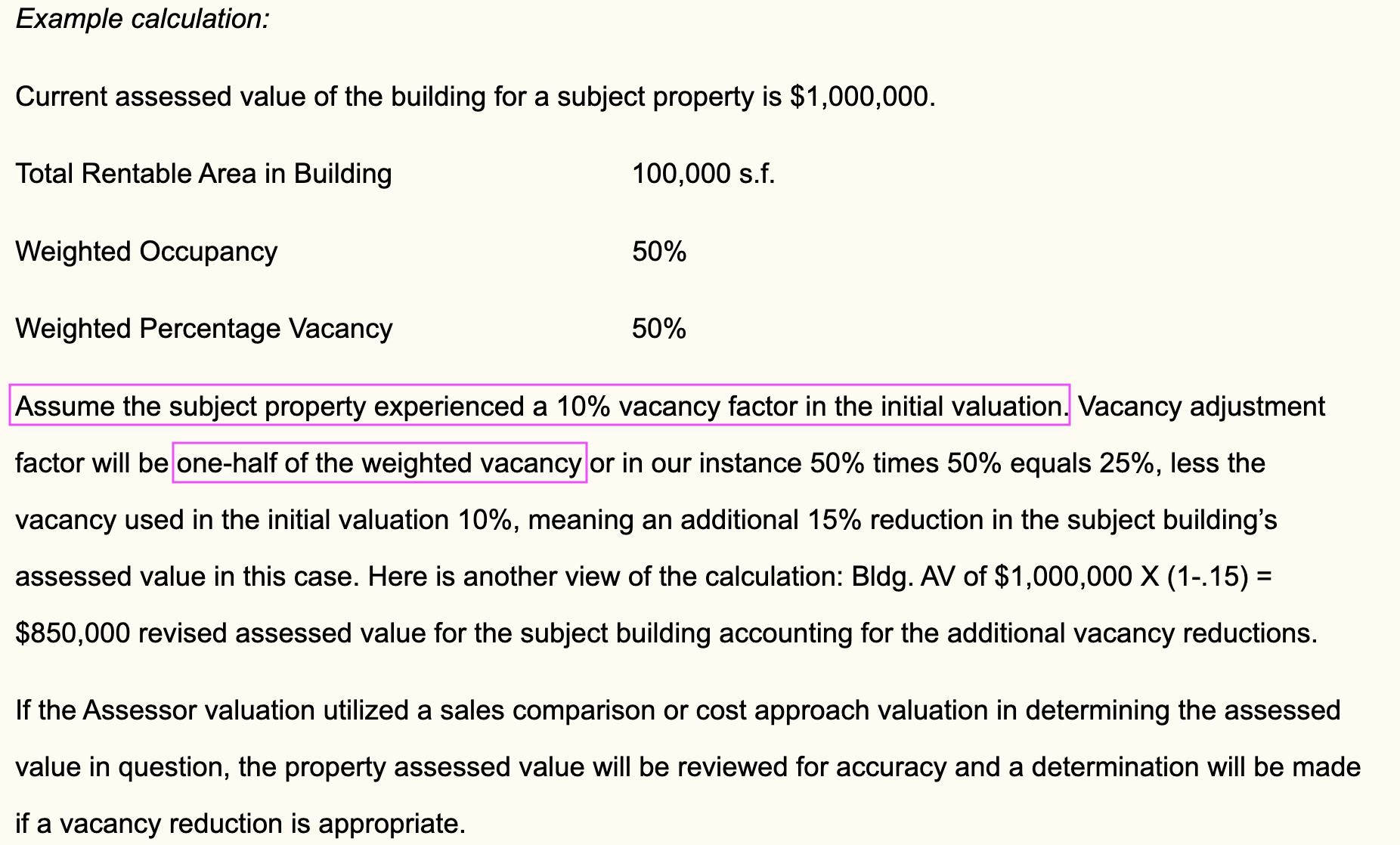

Cook County Assessor Vacancy Formula:

Below is the formula for which the Cook County Assessor grants tax relief based on vacancy:

1/2 of weighted actual vacancy – initial vacancy rate = vacancy reduction rate

Land Av + Building Av * (1 – vacancy reduction rate) = Total Av * (100/Assessment Percentage Rate) = Total Assessment Fair Market Value

Appellant Vacancy Formula for Relief:

The example property below conveys the formula that may be used upon appeal.

Other:

Miscellaneous reasons such as class change, error in characteristics, new construction cost, environmental contamination, and etcetera.

Peace Out.

###

Hire Us to Handle Your Appeal

Want experts to handle your tax appeal for you? We work on contingency, so you only pay if we win. There’s no risk and $0 required upfront.

Work With Us

Want to help property owners reduce their tax burden? We train practitioners and provide cutting-edge software tools to help you succeed in this industry.

The Real Estate Tax Newsletter

Get exclusive updates, insider strategies, and expert insights on real estate tax appeals delivered straight to your inbox. Whether you’re a property owner looking to cut costs or a professional in the industry, our newsletter keeps you informed and ahead of the game.

✔ Pro tips for lowering your property taxes

✔ Breaking news on tax assessment changes

✔ Data-driven insights from industry experts

Join now and never miss a key update.

From Fortune 500 companies to boutique law firms, I’ve spent over a decade navigating the real estate tax world. Since 2014, I’ve been mastering the game, and now, through this blog, I break down complex tax concepts into plain English, giving you the knowledge you need to take control. No fluff, just value.