Chicago Vs. The Rest of Illinois:

In the state of Illinois the real estate property tax code basically addresses counties in one of two ways, In counties with less than 3,000,000 inhabitants (non-cook which are 101 counties) and those with more (cook which is 1 county).

Below are the steps to a simplified property tax cycle:

1.) Assessor applies an algorithm to mass-appraise property values.

In Cook County the Assessor formerly establishes value for real estate properties once every three years (triennially). In all counties outside of cook, the same goes but for once every four years (quadrennially).

2.) Assessments are published with a 30-day window to appeal

Whether it’s a triennial/quadrennial assessment year or not, the proposed assessment values are published annually thus triggering a 30-day appeal window.

In Cook County the assessment level is 10% of Fair Market Value (FMV) for residential property and 25% of FMV for commercial. Outside of Cook county the assessment level is 33% of FMV.

3.) Assessments are revised following appeals to the Assessor

If the subject property is within Cook County there is a formal appeal at the Assessor level, if it’s in a county outside of Cook an appellant may appeal informally with the township assessor of that county.

4.) Exemptions and incentives are approved by the Assessor

The most common real estate tax exemptions are as listed below:

- Homeowner Exemption

- Senior Exemption

- Senior Freeze (Low Income) Exemption

- Disabilities Exemption

- Returning Veterans Exemption

- Veterans with Disabilities Exemption

- Long-Time Homeowner Exemption

- Home Improvement Exemption

5.) Assessments are revised following appeals to the Board of Review.

The Board of Review hears appeals following adjustments by the Assessor.

6.) Equalization factor is calculated by the IL Department of Revenue after the Board of Review closes, thereby adjusting values to the 1/3 requirement.

The equalization factor is a multiplier used to ensure that the total equalized value, or EAV, of real estate property in all Illinois counties equals 33 1/3 percent of the fair market value. Each county is assigned its own equalization factor and it does not cause taxes to go up or down.

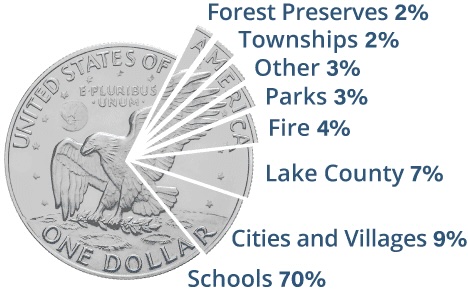

7.) Budget is set and the tax levy is established at the neighborhood level.

The school district comprises of the vast majority of the tax budget, while the police and fire department, amongst other services makes up the minority.

8.) Budget needs and the sum assessment values, per neighborhood, are used to determine tax rates

Property Tax Levy: Cook County proposes a total property tax levy of $803.8 million in FY2024, which is an increase of $20.7 million, or 2.6%, from FY2023.

Assessment Value * Tax Rate * Multiplier = Property Tax Bill per Property

The sum of all Property Tax Bills shall meet the Property Tax Levy.

9.) Tax bills are mailed and published on the Treasurer’s website

The annual property tax bill is separated into two installments. Cook County and some other counties use this billing method. Under this system, the first installment of taxes is 55% of last year’s tax bill. This installment is mailed by January 31. In Cook County, the first installment is due by March 1. (Elsewhere, a county board may set a due date as late as June 1.) The second installment is prepared and mailed around June 30 and is for the balance of taxes due. The balance is calculated by subtracting the first installment from the total taxes due for the present year. The second installment is generally due August 1 or at a later date as set by the county.

Peace Out.

###

Hire Us to Handle Your Appeal

Want experts to handle your tax appeal for you? We work on contingency, so you only pay if we win. There’s no risk and $0 required upfront.

Work With Us

Want to help property owners reduce their tax burden? We train practitioners and provide cutting-edge software tools to help you succeed in this industry.

The Real Estate Tax Newsletter

Get exclusive updates, insider strategies, and expert insights on real estate tax appeals delivered straight to your inbox. Whether you’re a property owner looking to cut costs or a professional in the industry, our newsletter keeps you informed and ahead of the game.

✔ Pro tips for lowering your property taxes

✔ Breaking news on tax assessment changes

✔ Data-driven insights from industry experts

Join now and never miss a key update

From Fortune 500 companies to boutique law firms, I’ve spent over a decade navigating the real estate tax world. Since 2014, I’ve been mastering the game, and now, through this blog, I break down complex tax concepts into plain English, giving you the knowledge you need to take control. No fluff, just value.